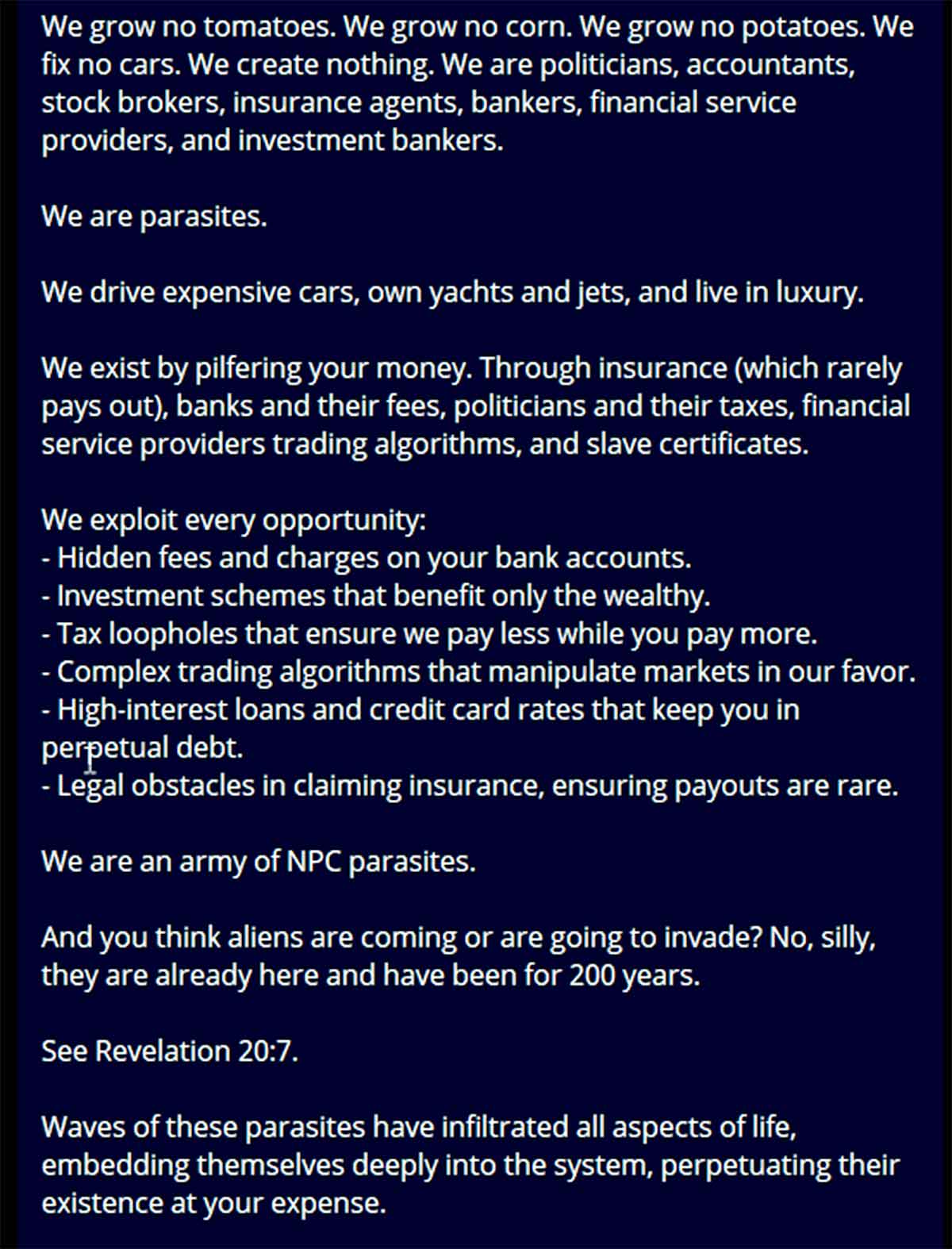

Home

Great World Reset

Website

Red Pilled Truthers

Website

click image for link to article

The day you retire

you become useless to a country –

and it certainly isn’t going to

invest in making your life a luxury

before you die.

Before your retirement ‘plan’

saw any of your contributions to it,

your ‘contribution’ was diminished by

the government in taxes,

the banks

and your financial advisers in annual fees

(that get paid whether you get anything or not)

and you got what was left over, if anything.

(That’s why unions got involved

in twisting members arms to have ‘Union’ super –

because then the union became the advisor

and collected the advisor fees) and is one of

the reasons unions are now worth $billions.

You’ve just turned from a person that sort of adds to the Gross Domestic Product of the country into something that will now become a liability.

You health will be deteriorating, you’ll require more medical attention, more ‘benefits’, more of everything.

Maybe even be entitled to a (gasp!),

a retirement pension.

You may think you paid for all this on the way to retirement during your working life with taxes – and besides you also managed to ‘save’ some as a ‘nest-egg’ to help you retire more comfortably.

And, as you settle down to relax

in what you think is going to be the

blissful retirement you think you’ve earned

for that bunch of years before you inevitably die

you’ll slowly work out maybe retiring

isn’t all it’s cracked up to be.

All those things in your bucket list you was going to do or places you was going to go suddenly seem terribly expensive and unaffordable.

Heck! even the heating and electricity and water bills and council rates and car registration and insurance now seem to be like paying the National debt.

And don’t make the mistake of eating anything decent – the supermarkets have got that covered too.

And if you ‘qualify’ for a pension

it must mean you’re broke.

Not only that, you’ll have to bare your entire financial affairs to a snot-nosed individual a fraction of your age who, you’ll work out, is paid to find a reason to NOT give you a pension – or at the very least reduce whatever you get to as little as possible.

And your pension will be reduced by any interest you get on any ‘savings’ you have – whether you get any interest or not – using DEEMING.

Make no mistake – if you retire with any kind of ‘nest-egg’ the government WANTS IT.

That is if you was relying on that compulsory ‘saving’ you had taken from whatever income you earned.

You made the mistake of thinking

you was ‘saving’ for your retirement.

What you didn’t realise is you was actually ‘investing’ in it – or, more accurately ‘gambling’ on it.

You’ll come to realise that you’re now considered to be an old-fart in gods waiting room – you’ll have no relevance, no say, no respect from anyone – other than maybe direct family or friends.

But the ‘system’ wants to rid itself of you as quickly as it can move you on.

And, if you happen to leave quickly, without spending all of your savings, so much the better – because then it can hit your estate for more tax.

For those who do make it in what they think is a relatively health financial situation, they’ll fairly soon find out the savings they could have spent 40 years ago might have actually been more useful then.

Because they’re not worth much now.

In fact trying to fund today’s lifestyle with yesterdays money is an exercise in futility.

And it also doesn’t take long to realise the only benefit a retirement savings plan has is to the government that forced you to put into it and to advisers that suck fees out of it.

(Which is WHY you was forced to put into it), and the organisations that ‘invested’ your money – without any input from you – on your behalf with their fees paid by you regardless of whether you made any money or not.

And mostly, you didn’t.

Your nest-egg was their nest-egg.

Notice whenever you see a

chart image about investments –

they always go UP?

It’s brainwashing.

You don’t want to believe this,

do you?

Ask yourself the question

‘if business is so ‘booming’

how come so many business’

are going down the toilet?’

📢📢📢📢

Be sitting down,

this is bad,

really bad …

PENSIONS

The ‘states’ have put

everyone’s house up as collateral

INCLUDING YOURS

on bonds that they leveraged 20 to 1

then stole the money

This means they BORROWED 20 million

for every 1 MILLION they had in tax revenue

and put YOUR house up as collateral to

repay it – which they NEVER would

This article/report is from USA

but do you think for one second

this isn’t the same in

EVERY country on Earth?

Found in at least Texas, Florida and Maryland – what state and local governments have done is borrowed 20 to 1 against your home property tax revenues.

They have been fraudulently inflating home values – 40% overvalued even – by just putting a few thousands of them on a spreadsheet, working backwards to figure out how much they want, then using those to do standard deviation/comparables, to determine appraisal values of homes across the area.

Effect: fraudulent, dramatic increases in tax appraisal values where of course your property tax bill skyrockets.

A govt. entity such as a school wants a new building, bam! no problem as they use the tax streams from all your homes, say it is $1 million, to go out and borrow $20 million.

Highly leveraged!!!

And where does this money come from?

Your pensions.

Now rinse and repeat. Remember the rates going up based on fraudulently inflated appraisals due to made up comps…..where now instead of $1 million tax revenue there is $1.4 million.

What does the State and local govts do?

Go out and borrow more using leveraged bonds.

Where is this money coming from?

Your pensions.

Including teacher pensions.

It is a vicious cycle including the crooks in the state and local govt. repeating fraudulently inflating property values again, and again and again.

Your property tax rates keep going up, they have been doing it for years.

The kicker: hundreds of billions of bonds are coming due, no one really knows how big this is.

Your property tax revenues have been spent for decades in the future….and that money is gone.

In Texas alone there are $32 billion in bonds coming due in 12-18 months.

And, $30 billion in mortgages due in the same time frame.

There is no money to pay them off.

And now it is being exposed all those billions were obtained via fraud – who is going to want to refinance those?

The only solution to what is coming is either property taxes skyrocket even more!

Or, bankrupting of teacher pensions, other pensions, people losing homes because they cannot afford property taxes and school board bankruptcies.

As Draza Smirh stated “Now I think I understand why those school board races have been so important to control.”

I can’t remember how many times I have published and stated in interviews Smurfing is found even in some school board races – is this why?

To cover it.

I have no idea if this is connected but yesterday Warren Buffett is selling real estate investments, google it.

~ Peter Bernegger ~

click image for link to PDF

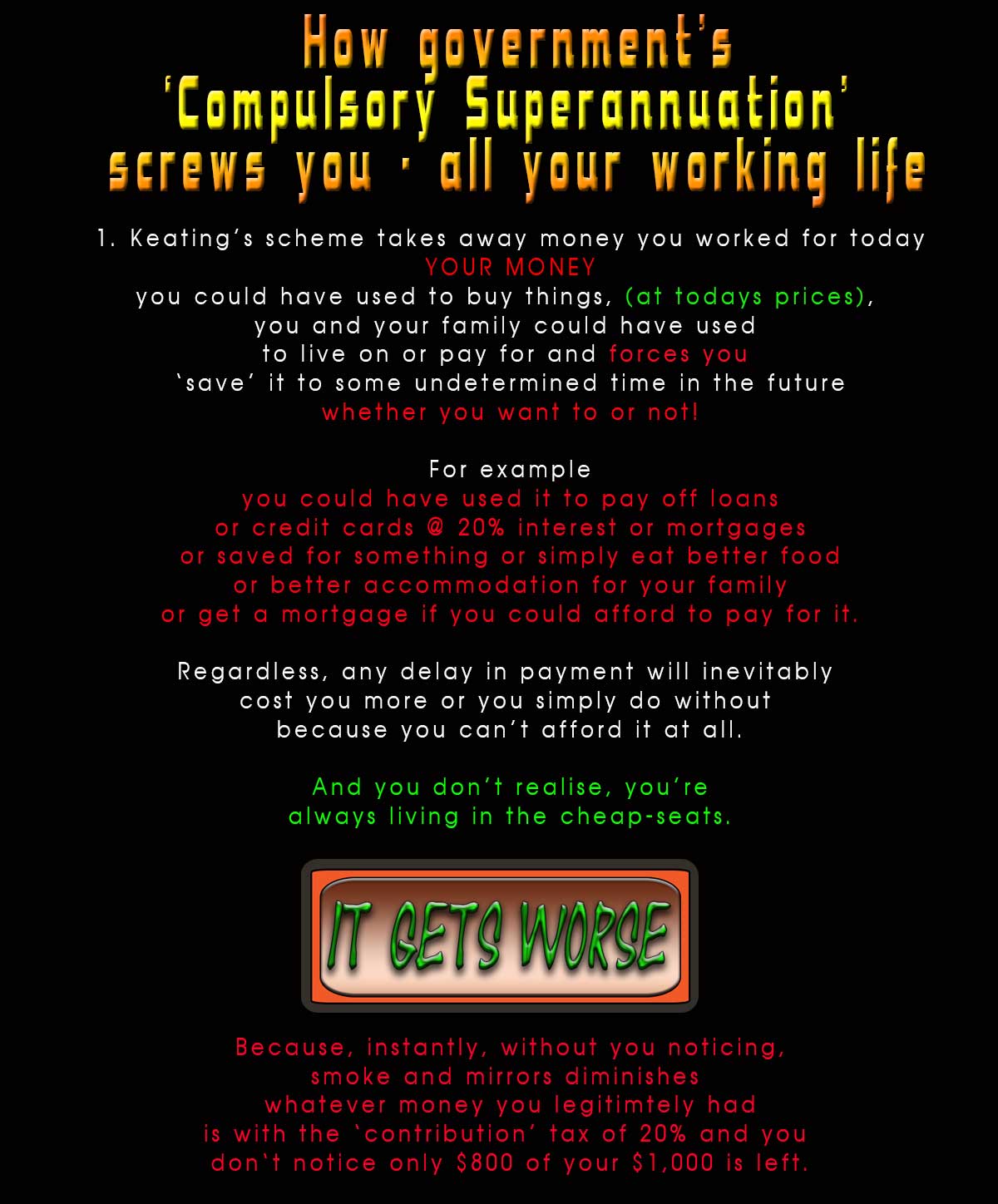

Seems Superannuation

is under attack (PDF)

from the Aus Government

Website (PDF)

Do the SUMS

for yourself

(they’re not hard)

Let’s say you put $1,000 ‘into’

your retirement-funding … ‘fund’.

First cab off the rank …

instantly …

you get hit for ‘contributions tax’

of 20%

before your money ever makes it

to your account

You’re now 20% light = $200

OK – lets take that remaining

$800

and see what happens to it in year 1

There will also be other fees the

fund will charge for ‘managing’ your money.

These fees will be taken in advance

Then there may also be additional fees

if you haven’t told the fund to not provide

life insurance and disability cover for you.

The premiums for this cover will be deducted

from your account AFTER the tax department

and the fund manager has been paid along

with any fees paid to any financial adviser –

which could be a union.

Likely the adviser gets a commission

from the insurer providing the life insurance,

(you may not want or need)

– on top of the other fees.

Now, what’s left of that $800,

(less the other fees mentioned),

is ‘invested’ for you.

The fees ALWAYs get paid first

and if your fund investment

‘growth’ doesn’t cover the fees

your account balance is diminished.

Even if it does ‘earn’ interest for you –

and it needs at LEAST 25% growth

($200) JUST to break even.

And it won’t.

It never breaks even –

as it will never earn 25% –

so your account balance

will only ever go backwards.

And then, there’s the hidden

compounding effect of inflation

Inflation and next years fees

will see to that

But, when you get your statement it will

LOOK LIKE you’re ‘making’ money.

HOW?

You get your statement well after the end

of the tax year – why?

So that years 2 ‘contributions’

can be added to the account balance,

often BEFORE the fees are accounted for.

So, your fund balance has increased

by last year’s ‘contributions’.

You get a statement.

You look at ‘start’ balance for the year

and the ‘end’ balance for the year.

The ‘end’ balance seems bigger than the ‘start’ balance –

so you stuff the statement in a shoebox

never to see the light of day again.

Until, one day, you staring down the barrel of retirement –

and all of a sudden that balance become really important.

By which time it’s too late

to do anything about it.

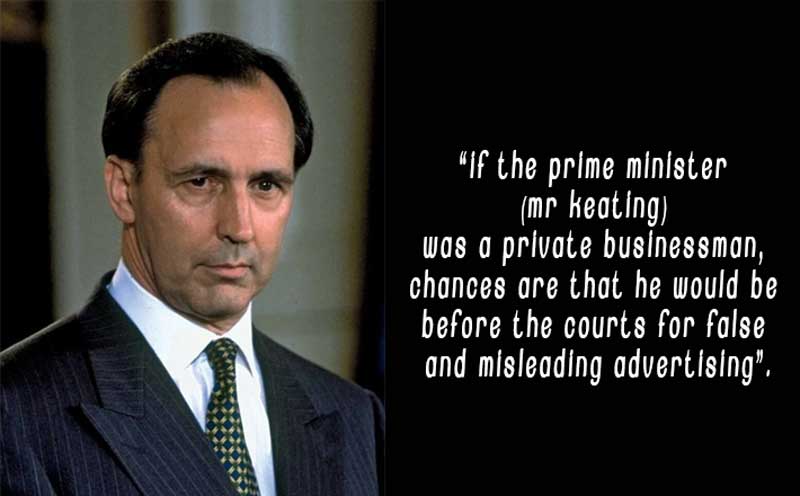

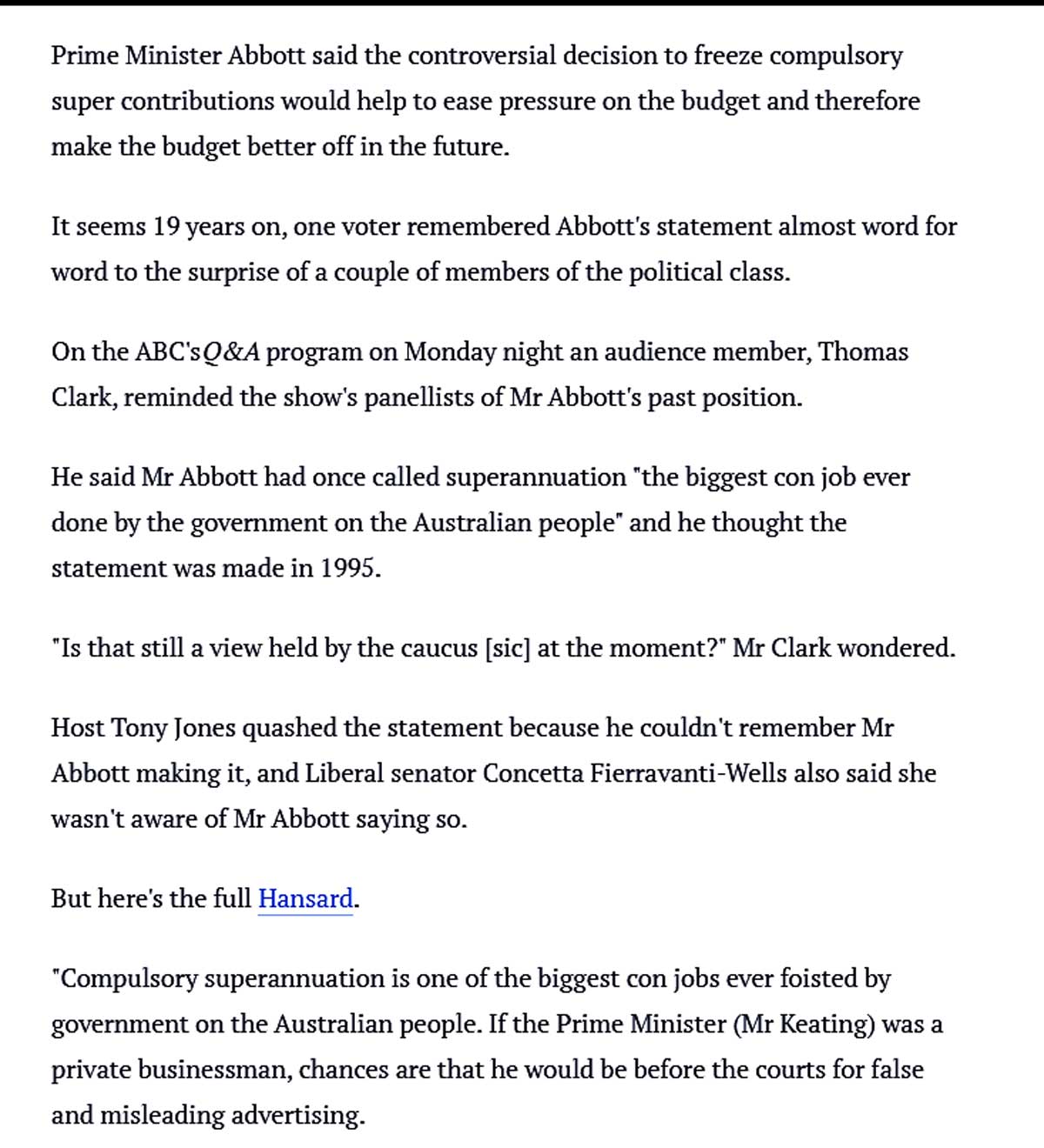

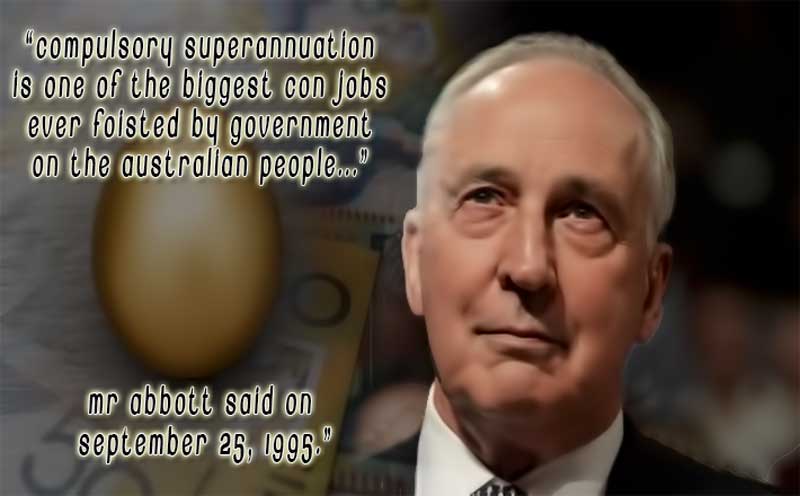

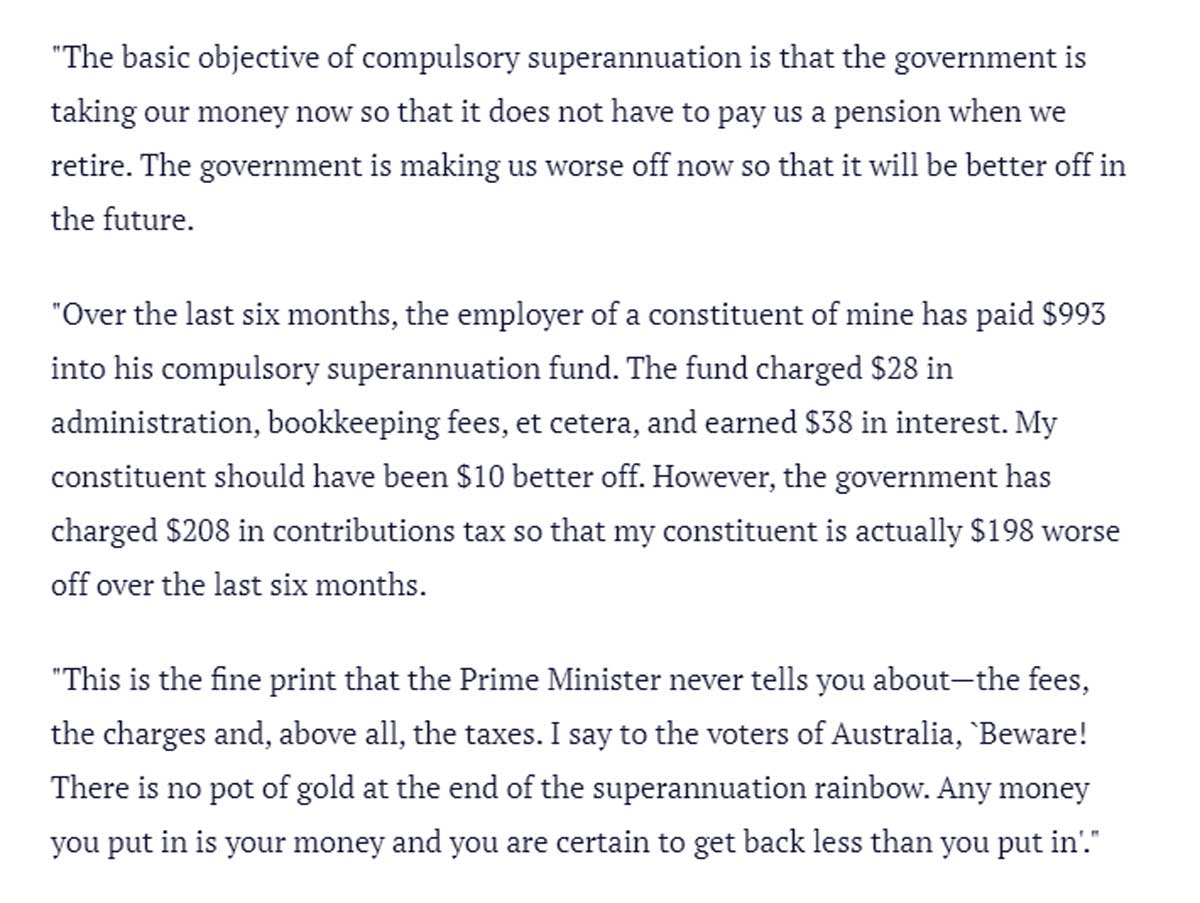

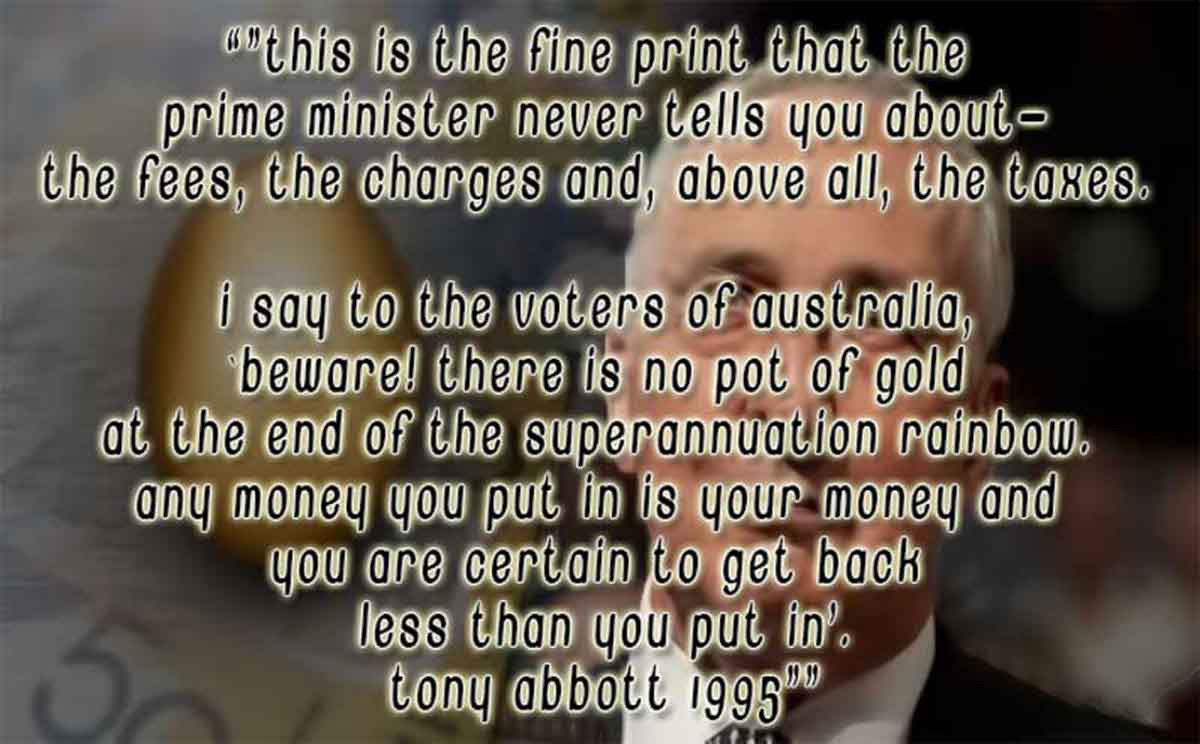

Tony Abbott DID try and warn people

but his message was silenced.

-0-0-0-0-

Now … get this

EVERY ‘contribution’ you EVER make

to your ‘super’ fund

is treated the same way.

NONE of them can EVER ‘catch up’

to the FEES they incur UP-FRONT

(and inflation) EVEN IF YOU

DON’T PAY FOR INSURANCE

Your ‘super’ fund will NEVER

actually EARN YOU ANYTHING.

All that happens is when you retire

if you’re lucky you might get BACK

pretty much what you’ve

‘contributed’on the way

(providing you started your

‘super’ plan at least about

30-years prior to retirement).

Then you get hit for ‘withdrawal tax’

on whatever’s left.

click image for link to article

Beginning to get it yet?

You would have been better off

if you’d not been in ‘super’

paid the tax and

kept the money to use yourself.

The government knows that you’ll

find this out so it made

Superannuation compulsory

and put the onus on your

employer to collect it.

click image for link to original article

A Proposal for Web3-Based

Universal Basic Income

Income and wealth distribution have become more unequal in both the advanced and developing worlds over the past two decades.

With automation poised to exacerbate this gap by replacing large numbers of certain jobs in the coming years, how to distribute social wealth to ensure the fruits of economic growth are more fairly shared will become an even tougher policy challenge.

Universal basic income (UBI) – a type of social-economic programme where all citizens of a jurisdiction regularly receive a monetary transfer, usually from the government, without discrimination – may provide an elegant solution to help address the issue.

Large-scale implementation of UBI on a national level, however, may require further innovations on both technological and economic fronts.

This paper lays out a proposal for leveraging web3 technologies – digital transaction networks such as blockchain or other programmable ledgers – as the infrastructure for scalable and efficient UBI implementation.

This website is always

'work in progress' and your

contributions, corrections and

suggestions are invited

Please report broken links

Send files or messages direct to

redpilledtruthers@gmail.com

... this website does not collect

any information or leave cookies

email: redpilledtruthers@gmail.com

Contact Red Pilled Truthers